Chasing Gold: The Incredible Story of How the Nazis Stole Europe's Bullion (26 page)

Read Chasing Gold: The Incredible Story of How the Nazis Stole Europe's Bullion Online

Authors: George M. Taber

BOOK: Chasing Gold: The Incredible Story of How the Nazis Stole Europe's Bullion

9.5Mb size Format: txt, pdf, ePub

The New York Federal Reserve balance sheet of September 30, 1939 showed that thirty-nine countries had parked some of their national gold in the vault in lower Manhattan.

14

It was arriving so fast by April 1940 that the New York Fed decided to begin charging for services that had up until then been free as a gesture of good will among central banks. The Fed now charged 33.5704 cents for each gold bar received and 22.6007 cents for each bar sent to the Assay Office to test its purity.

14

It was arriving so fast by April 1940 that the New York Fed decided to begin charging for services that had up until then been free as a gesture of good will among central banks. The Fed now charged 33.5704 cents for each gold bar received and 22.6007 cents for each bar sent to the Assay Office to test its purity.

Shortly after the Germans took over the Czech rump state of Slovakia in March 1939, President Roosevelt asked Morgenthau to look into what actions the administration could take to help the Allies get more weapons without asking Congress again for new trade legislation. The Secretary assigned Harry Dexter White, his top aide, to come up with a plan for waging economic warfare on Germany. On April 8, 1939, White presented a preliminary report on “the possibility of depriving the aggressor countries of needed strategic war materials.” The study zeroed in on nine products that were vital for war, but which Germany had in only short supply. They were: manganese, copper, tin, rubber, petroleum, nickel, manila fiber, tungsten, and cotton. White estimated that Germany had to spend $100 million a month to import the commodities needed to keep its war machine running.

15

15

White did not yet realize that the Nazi strategy was to pay for those products with gold stolen from its victims. White proposed purchasing stores of the strategic materials to keep them out of German hands or establishing international agreements to stop the Nazis from getting them. Morgenthau asked the president to support a billion-dollar program to buy up the three most strategic products: oil, tin, and manganese. After consulting with his war, navy, and state departments, though, Roosevelt decided that the price tag was too high, and the administration eventually asked Congress for $10 million, a fraction of what was needed to do the job.

16

16

Following the invasion of Poland on September 1, 1939, however, the Roosevelt Administration moved with a new urgency to help the western allies militarily even though the American public still opposed entering another European war. The Neutrality Act of 1935, which had been regularly renewed with only minor changes, imposed an embargo on all war materials and to all parties in the conflict. On September 21, 1939, the president asked Congress to replace that with a new policy that became known as Cash and Carry. It would allow arms sales under stiff conditions. The primary ones were that the buyers had to pay immediately in convertible currencies or gold and had to provide their own transportation for their purchases. Moreover, foreign vessels picking up military hardware could spend only twenty-four hours in a U.S. harbor. Since it often took longer than a day to unload gold and then load heavy equipment such as airplanes, the western allies used Halifax, Canada as a drop-off and pick-up harbor. Vessels brought gold from Europe destined for the New York Federal Reserve and picked up war goods. Cash and Carry was designed primarily to help Britain and France. The new proposal passed Congress relatively quickly and became law in November.

On February 5, 1940, Harry Dexter White informed Morgenthau that France and Britain would soon buy $1 billion worth of airplanes and spend even more on other weapons. He added that they still had $14 to $15 billion in foreign exchange assets, but warned that at the rate they were purchasing they might spend half of that within a year. White speculated that each had left roughly $6.5 billion in gold.

17

17

Morgenthau began getting regular reports on world gold shipments from the New York Federal Reserve. The inflow to the U.S. had been only about $100 million per year in the 1920s and early 1930s, but in 1935 had jumped to $1.7 billion, and in 1939 was likely to hit $3 billion. On Tuesday February 6, 1940, the U.S. bought $22.5 million in gold from the Bank of England, $1 million from the Dutch, and $410,000 from Belgians for a total on that one day of $23.9 million. An additional $3.2 million came via Canada. The Fed received a cable from the Bank for International Settlements to transfer $2.7 million from its account to the Turkish National Bank. The traffic was staggering:

• The Bank of Iceland sent $800,000.

• The Bank of Latvia sent $11 million.

• The State Bank of the U.S.S.R. on September 27, 1939, sent 160 bars of gold via San Francisco.

• The Bank of Romania in late December 23, 1939, sent $845,486 and on March 5, 1940, another 84 more bars worth $1.2 million.

• The Bank for International Settlements in the fall of 1939 made two shipments to New York worth $6.3 million.

• The National Bank of Hungary in late February 1940 sent $3 million.

• The Ministry of Foreign Affairs of Afghanistan even contacted the U.S. embassy in Paris to ask about the New York Fed’s gold policy.

18

By the fall of 1939, it was hard to shock the U.S Treasury policymakers, but in November 1939 the British Exchequer stunned even Treasury Secretary Morgenthau by selling $50 million more in gold. Between the beginning of the war in September 1939 and early 1940, British gold sales amounted to $125 million, and the sales of securities were $112 million.

19

19

The Scandinavian countries were particularly nervous about being invaded and losing their gold. Sweden took the lead, and its central bank president Ivar Rooth often spoke for other Nordic central banks. He sent messages to New York City for the Danish Central Bank, asking if Finnish gold could be sold for delivery in Stockholm. The Federal Reserve said no. It did not want to take the added risk of getting it from Stockholm to New York. In February 1938, Rooth sent a letter to New York Fed president George Harrison, saying that he had “long contemplated to distribute gold holdings belonging to the bank.” Sweden had significant deposits in London, but he wanted to move them out of harm’s way. As war dangers increased, the Swedish banker was soon shipping large amounts of bullion to New York at his own cost. In June and July of 1938, he sent $15 million on four separate sailings. In October 1939, he transferred $25 million and then in December another $5.9 million. A week before Christmas in 1939, Sweden’s Rooth sent a year’s end message to the New York Fed’s Harrison, “We must also think of the possibility that we might become the next victim of the Russian bear. We pray for peace in 1940, but we prepare for the worst.”

20

20

By the early months of 1940, the influx of gold into the U.S. from Europe was so great that there was a risk that it could destabilize the international monetary system. More than sixty percent of the world’s gold was now in the U.S., as compared to twenty-three percent in 1913 or thirty-eight percent in 1929.

21

In the spring of that year and with that trend only growing greater, Morgenthau asked Harry Dexter White to work on a major study on the subject. He called his long report “The Future of Gold.” The Treasury Secretary had been invited to give a talk to the Women’s Division of the Democratic National Committee, and he hoped that his aide’s work might make its way into the speech. The professor came out in White’s work, however, and the study turned out to be akin to an academic treatise. At one point, though, he alarmingly wrote: “Suppose the war lasts more than three years? Suppose it lasts five years? At the rate gold is now coming in—$2 billion to $3 billion a year—we would assuredly have most of the world’s gold by the end of the war.” White also delved into the future of the world monetary system. In many ways, he was exploring issues that would be the basis for the 1944 United Nations Monetary and Financial Conference that was held in Bretton Woods, New Hampshire near the end of the war that was then just beginning.

22

21

In the spring of that year and with that trend only growing greater, Morgenthau asked Harry Dexter White to work on a major study on the subject. He called his long report “The Future of Gold.” The Treasury Secretary had been invited to give a talk to the Women’s Division of the Democratic National Committee, and he hoped that his aide’s work might make its way into the speech. The professor came out in White’s work, however, and the study turned out to be akin to an academic treatise. At one point, though, he alarmingly wrote: “Suppose the war lasts more than three years? Suppose it lasts five years? At the rate gold is now coming in—$2 billion to $3 billion a year—we would assuredly have most of the world’s gold by the end of the war.” White also delved into the future of the world monetary system. In many ways, he was exploring issues that would be the basis for the 1944 United Nations Monetary and Financial Conference that was held in Bretton Woods, New Hampshire near the end of the war that was then just beginning.

22

Morgenthau met with White in Sea Island, Georgia in the spring to go over his work. The secretary reiterated his support for gold, saying that he “felt it did not matter whether the government was a democracy or a totalitarian government or whether its economy was socialism or free enterprise, it would still use gold for international transactions.” White agreed. The two concluded, though, that White’s work was too dense and theoretical for Morgenthau’s upcoming speech and would go over everyone’s head including his own. So the secretary’s staff produced a more popular talk that stressed the strength of the U.S. economy and the role of gold. The secretary gave his talk in Washington on May 3, and it received good press reviews, which pleased him because he was not a natural public speaker and rarely spoke at public forums. Emil Puhl, the new power at the Reichsbank after the ouster of Hjalmar Schacht, read a copy of the speech and wrote a letter to the U.S. financial attaché in Berlin about his own views on bullion: “I am personally of the opinion that the role of gold in the monetary respect need not by any means have been played out provided all parties concerned can arrive at a reasonable solution of the gold problem.”

23

23

After his speech to the Democratic women, Morgenthau left for an R-and-R visit to Chicago. At 3:00 on Sunday morning May 5, he woke up and scribbled a note to his secretary on a small pad supplied by the Shoreland Hotel, where he was staying. He noted the date and time and then wrote: “Please tell Dan Bell I want enough money to move all the remaining gold out of N.Y. City to Kentucky. He should speak to me Tuesday.” Morgenthau underlined the word “all” three times and put his initials at the bottom. In the morning his son asked why he had gotten up in the middle of the night and written a note.

24

24

Two days later, Morgenthau was back in his Washington office. At his regular morning staff meeting he explained his middle-of-the-night note, saying, “I got to worrying about three or four billion dollars worth of gold laying in New York.” Undersecretary Dan Bell explained that Fort Knox had the capacity to hold about $15 billion dollars in gold, but was only about one-third full. He figured it could store at least $9.5 billion more. Bell proposed sending about $7.5 billion to Kentucky. An irritated Morgenthau replied that he wanted to ship $10 billion, adding, “I will take it over to the president myself. It is the height of stupidity when it cost a million and a half dollars not to remove ten

billion

dollars to a place of safekeeping.”

25

In his memo to the president Morgenthau recommended that “in the current calendar year” the government should ship “approximately $9 billion of refined gold from New York to Fort Knox. He estimated that this would require a supplemental budget appropriation of $1.6 million. Roosevelt approved the proposal.

billion

dollars to a place of safekeeping.”

25

In his memo to the president Morgenthau recommended that “in the current calendar year” the government should ship “approximately $9 billion of refined gold from New York to Fort Knox. He estimated that this would require a supplemental budget appropriation of $1.6 million. Roosevelt approved the proposal.

Morgenthau learned that same day that the treasury had just received $21.8 million in gold from Canada, Britain, Switzerland, and Portugal. In addition the Netherlands had wired that it would be soon sending $3.7 million more. Nazi propaganda claimed that the U.S. was simply trying to grab all of Western Europe’s gold, and the British press also angrily reported that the U.S. now had seventy percent of the world’s bullion.

26

The Bank of England had previously been the major location where countries parked their bullion for protection, but with London no longer looking like a safe location, it was now going to the U.S. Large shipments from Switzerland, Sweden, and Portugal landed at the New York Federal Reserve for safekeeping, and it was sometimes gold that they had received from Germany. Without realizing it, the U.S. was actually helping finance the Nazi war effort by giving Hitler’s partners a secure place to store stolen bullion.

27

26

The Bank of England had previously been the major location where countries parked their bullion for protection, but with London no longer looking like a safe location, it was now going to the U.S. Large shipments from Switzerland, Sweden, and Portugal landed at the New York Federal Reserve for safekeeping, and it was sometimes gold that they had received from Germany. Without realizing it, the U.S. was actually helping finance the Nazi war effort by giving Hitler’s partners a secure place to store stolen bullion.

27

The national press was slow to pick up on the historic influx of gold to the U.S. In June 1940, though, the papers finally paid attention. The

New York Times

and the

Washington Post

carried breathless headlines such as “May Gold Imports Double; Britain Ships Heavily,” “Half Billion of European Gold Enters U.S. in 2 Days,” and “$225,000,000 in Gold Arrives Over Week-End.” The Nazi invasion of the Low Countries and France had precipitated the latest panic. The

New York Times

in a story datelined June 4 reported, “One of the greatest mass movements of gold in history is now under way.”

28

New York Times

and the

Washington Post

carried breathless headlines such as “May Gold Imports Double; Britain Ships Heavily,” “Half Billion of European Gold Enters U.S. in 2 Days,” and “$225,000,000 in Gold Arrives Over Week-End.” The Nazi invasion of the Low Countries and France had precipitated the latest panic. The

New York Times

in a story datelined June 4 reported, “One of the greatest mass movements of gold in history is now under way.”

28

A series of memos the Treasury staff sent to Secretary Morgenthau showed starkly how the U.S. was gathering up nearly all the world’s central bank gold. One on July 1, 1940, reported that the U.S. during the previous month had purchased $662.8 million, with $242.7 million of that coming from Britain and $332.9 million from France. Moreover, it stated that in the ten months between September 1939 and June 1940, those two European countries had sold the U.S. $1.7 billion in gold (France $900.7 million, and Britain $766.8 million). At 2014 prices, that would have amounted to $60 billion.

29

29

In the first full year of World War II, from September 1, 1939 through August of 1940, the U.S. took in $4.1 billion in bullion from mainly European countries. Harry White noted in a report in late September 1940, “This is by far the largest sum of gold ever received by us or any country in a like period. We now have slightly over 70 percent of the monetary gold held by governments and central banks. We actually hold 80 percent of the world’s monetary gold if we include earmarked gold held here.”

30

30

On October 28, 1940, Henry Morgenthau wrote in a memo that London had just ordered $1.6 billion in war materials and was preparing for an additional one of $3.3 billion. Unless there was a change in American policy, the purchases would all have to be paid for in gold.

31

31

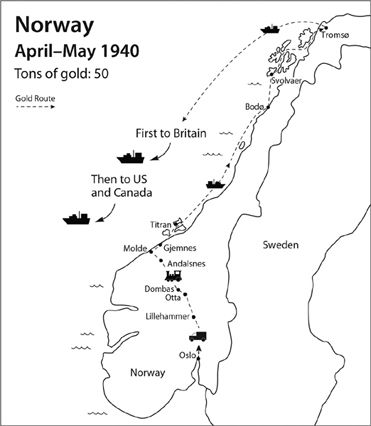

Chapter Thirteen

DENMARK AND NORWAY FALL QUICKLY

Other books

West of Here by Jonathan Evison

The Wedding Affair (The Affair Series Book 2) by Suzanne Halliday

Deep Sea by Annika Thor

Eden's Eyes by Sean Costello

Merciless Ride by Chelsea Camaron

Initiate Me by Elle Raven

Captivated (The Dragons) by Elias, Ella

Touch of Amber: Hot Rods, Book 7 by Jayne Rylon

Water For Elephants by Sara Gruen

Fever Claim (The Sigma Menace) by Marie Johnston