I'm Only Here for the WiFi (13 page)

Read I'm Only Here for the WiFi Online

Authors: Chelsea Fagan

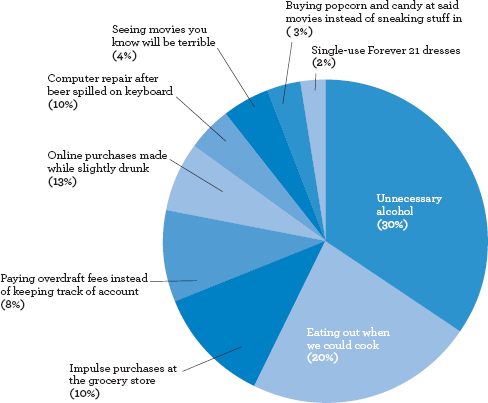

Transport is but one lowly example of the kind of blockades that are set up throughout a young adult's life to prevent him from living in financial equilibrium. It seems that everywhere you go, there is a new thing to do or a new way to do it, something that everyone is doing that you now need to be doing as well. You face unintended expenses, rising rents, and friends who are all going out, and you run the risk of looking like a cheap jackass if you do not join them.

â¢

Having to attend multiple birthday parties for friends that are held in places like restaurants and bars, where the food and drink are devastatingly far from being free. (Unlike a regular night out, a birthday night is one that you can't just delicately decline and pretend as if nothing happened.)

â¢

The aforementioned taxis to and from almost every event that either requires crippling “going out” shoes or ends at an unreasonable hour.

â¢

Offering a round for everyone while you're out, which you can by no means afford, but which seems like a good idea when you are in the “I am literally made of $100 bills” stage of your drunkenness.

â¢

Delivery food when you can't motivate yourself to look like enough of a human being to go outside.

â¢

Getting a real meal at lunch during work, instead of packing yourself something both nutritious and affordable, as you know you absolutely should be doing.

â¢

Realizing that you are now, as an adult, required to get everyone gifts at holidays, instead of just receiving them like some childish vacuum of materialism. (This is also often the moment where you realize that Christmas is less fun when you're paying for a significant part of it.)

â¢

Travel to go see people who have magically migrated out of your life/geographical region upon graduation.

â¢

Weddings. (Ugh, weddings.)

â¢

Random shopping purchases that you make because you either want to cheer yourself up or crumple entirely under the steely gaze of an overly aggressive salesgirl.

â¢

Purchases that, while not so random, are way beyond your means. There is a difference here between buying a $10 shirt at H&M and buying the exact same shirt in form and function for $300 because you think it looks cool. (Spoiler alert: It never looks

that

cool.)

â¢

Rent which, by being in an incredibly expensive city that you “have” to live in because it is the “best city ever,” basically beats your checking account into an unrecognizable pulp once a month.

â¢

Keeping up, in one way or another, with friends who are very far away from your financial laneâwhether as a result of their own successes or parental subsidies.

â¢

Diet/exercise/fitness products that you will use/eat/try about three times before promptly abandoning them, regardless of cost.

â¢

Beauty/skin/hair care products that only get more complex and expensive every year.

And these are just some of the more egregious offenders. The truth is that a huge number of the expenses of our daily lives are nothing more than that: innocuous, everyday things. We simply never imagined that we would have to buy them. Few things can quite re-create the sinking, slowly forming depression brought on by realizing that you have to buy things like toilet paper and soap, regularly, all by yourself, for the rest of your life. Things like this always seemed like constants, like something that would just appear in your cabinetsâor, at the very least, not cost so much. But they are incredibly expensive, and often have to be organized into a system of importance in which they fall toward the top when the end of the month comes around. Because no matter how many times we insist that we are spending less this time, until we make a firm budget and stick to it, getting through the month with a decent amount of savings and no stomach-churning “How am I going to eat?” feelings is not a possibility.

Real budgets, however, have always seemed like the stuff of adults much older than we'd ever imagined ourselves being. People with children, and mortgages, and spouses, and subscriptions to cheese-of-the-month clubsâthose are the kinds of citizens who keep their monthly spending neatly organized in an Excel spreadsheet. But there will come a point, without exception, when you realize that you need to have one of these budget things for yourself. This may be difficult to admit, because it implies not only that you are now in an age bracket that is

entirely responsible for its own financial future, but also that you have become boring enough to take it seriously.

When you're twenty, there is only “money,” and that exists in a kind of nebulous pile in the back of your mind. Much of it is fake, school loan money that you know will one day have to be repaid, but can't imagine actually dealing with. And there are, of course, your parents, who are usually there to help you to some degree. While we all have our varying combinations of “disposable income” and “personal responsibility,” rarely do we think in the long term. You have money, and then you don't. It's not a matter of “making it work for you,” because how could it? When you're busy taking out as much of it as bank officers will hand you in between cleaning their bifocals, how can you pretend that you are taking the reins of your future firmly in your semiadult grip?

In the interest of full disclosure, I got off quite lightly on the whole student loan front. I have my debts that I'm grudgingly paying off, to be sure (including, but not limited to, the extremely misguided Visa I procured at the ripe age of eighteen and proceeded to max out in a matter of days), but I have it pretty good compared to many of my peers. Many among us are looking at debt that is in the upper five figures, if not more. And while there is no shame in struggling with the unfortunate decisions of our freshly-accepted-to-our-dream-school selves, it certainly makes the whole situation exponentially more difficult.

So how do you make a budget? Speaking as someone who has

only very recently created a somewhat coherent monthly schedule of income and expenses that includes actual bill paying and not simply dodging phone calls, as well as putting things aside for a future that may include one day owning something instead of just renting it for an extended period, I feel on shaky ground at best to offer a foolproof plan. But from frustrating experience, I know that certain things do not work. You can shoot yourself in the foot, as with some of the purchases previously listed, but there are also more insidious ways of sabotaging what would otherwise be a healthy relationship between money taken in and money put out.

Don't avoid looking at your bank or credit card statement. It may be tempting, I know, not to check the damage after a particularly fruitful night out or a bout of bill paying that leaves you feeling at once relieved and depressed, but you have to. Aside from the possibility of your card (or card number) having been stolen in one of your less lucid moments and your remaining blissfully unaware of the new purchases, it is always important to know the particulars of your financial status. The difference between going for the luxurious chicken pesto wrap at your local organic deli and picking up a cup of ramen from the corner store could be a few dollars that you only imagine you have. Sure, it does mean encountering those stomach-dropping moments of “Oh, my god, where the fuck did all my money go?” on a more regular basis, but it will avoid a bigger, more long-term disappointment when you finally hold your eyelids open and force yourself to look at your bank statement.

Don't make big purchases without planning for them. Coming

from someone who once bought an IKEA couch while in a drunken stupor, staring at my half-broken futon that I hated so much I could not go another day without replacing it, planning is key. Whether it's a coat you've been eyeing forever, a new piece of furniture, or just a plane ticket that is so frustratingâcome on, you're just sitting in a flying tube for a few hours, why is it so expensive???âyou need to do some serious preparation. Even if you're the cool, spontaneous type who just likes doing things when the spirit moves you, including getting a new washing machine for your apartment, wouldn't you want to get it on sale? That's the thing about taking your time: So often you find that you could buy something you wanted for less money or that you don't need it at all. It's like waiting a minute and thinking about whether or not you really need those Mentos at the cash register, except the Mentos cost $500, and you don't even have that in your savings account right now.

Don't accrue overdraft fees. Motherfucking overdraft fees. My archnemesis, right after shower stall scum and when someone puts an empty bottle of milk back into the refrigeratorâoverdraft fees. What evil wizard concocted this ingenious plan, allowing unsuspecting bank patrons to spend all this extra pretend Monopoly money that they don't actually have in their accounts, problem-free, until they have to pay it back with added bonus insane charges on top of it that are not even remotely proportional to the purchase itself? You bought a pack of gum that puts you over your limit by sixty-seven cents? Congratulations, you get to pay

$35 for the privilege of not having that embarrassing “Your card has been declined” moment at the gas station cash register. Thank you, bank, for providing my worthless life with this incredibly useful service that doesn't at all ravage my already paltry bank account into a withered husk of its former self.

Don't compare what you have to others. This is simply a game that cannot be won. Whether or not you feel comfortable in your current financial bracket, there is always going to be someone who is better-off than you, has more access than you, seems to be more successful than you, or is capable of doing things you cannot. This is just a fact of life, and it's not going to change because you've figured out your flashy acquaintance's salary down to a $5,000 range by looking up his job online. Chances are that he is, indeed, making much more money than you are. Does this mean that he is happier? Maybe, maybe not. But it's not as though your obsessing over not measuring up is going to suddenly make your boss burst into your office one day and announce via megaphone that you are getting a brand-new salary of $500K a year, plus signing bonus, effective immediately.

Don't stray from your financial lane. If you can afford something, awesome for you. You should integrate said thing properly into your budget and then buy the shit out of it. But if you cannot afford this item or trip or night out at the club, pretending you can afford it to hang out with certain people or give a certain appearance is never a good move. Where do you think all this imaginary

money is going to come from? It's either getting sucked directly out of your bank account, where it would have otherwise been used for such necessities as paying bills and eating, or it's going to be put on a credit card. The last thing any of us needs right now is accruing credit card debt over buying a $500 jacket or an entire bottle of champagne at a table in a nightclub. Sure, it's always uncomfortable to have to be like, “No thanks, friends, I would love to join in with this, but alas, I cannot afford it.” But no way is that more uncomfortable than realizing you have to subsist on cardboard boxes for the last three days of the month.

There are clearly things to avoid, things that are obvious red flags away from which we need to steer our respective piles of money. But a budget is so much more than just

not

doing certain things; you also have to tackle the whole constructing-an-actual-plan-of-some-kind-for-your-everyday-and-long-term-spending that has to go along with it, which is often more difficult. And the foundation on which to base our budgets often ends up being however much money we are able to get out of our jobs. With many of us still languishing in exploitative, unpaid internships, though, how do we command a salary? How do we determine what we are worth?

Speaking as someone who has pretty much never negotiated for paymentâexcept once when I meekly suggested a fraction more to cover transportation costs and promptly apologized for asking when I was given a firm “No”âI know it's hard. But how

else are you going to develop a budget if you don't have a place to start? And the truth here is that you just have to demand a certain amount for yourself. If you are in your twenties, no matter how glamorous or desirable the industry, you cannot allow your youth to be sucked out of you through a crazy straw in some glamorized intern position. While supplementing your hours waiting tables, or babysitting, or even taking a job in a less sexy field is never anyone's first choice when drawing What I Want to Be pictures when we're five, sometimes it's just necessary. After all, if you're living in one of the most expensive cities in the Western Hemisphere, it's better to be managing your professional expectations than to be sharing a studio apartment with four smelly graduate students who steal your leftovers out of the fridge.