The Gardens of Democracy: A New American Story of Citizenship, the Economy, and the Role of Government (9 page)

Authors: Eric Liu,Nick Hanauer

Tags: #Political Science, #Political Ideologies, #Democracy, #History & Theory, #General

BOOK: The Gardens of Democracy: A New American Story of Citizenship, the Economy, and the Role of Government

2.37Mb size Format: txt, pdf, ePub

You might think that this shift in metaphors and models is merely academic. Consider the following. In 2010, after the worst of the financial crisis had subsided but still soon enough for recollections to be vivid and honest, a group of Western central bankers and economists got together to assess what went wrong. To one participant in the meeting, who was not a banker but had studied the nature of economies in great depth, one thing became strikingly, shockingly clear. Governments had failed to anticipate the scope and speed of the meltdown because their model of the economy was fantastically detached from reality.

For instance, the standard model used by many central banks and treasuries, called a dynamic stochastic general equilibrium model, did not include banks. Why? Because in a perfectly efficient market, banks are mere pass-throughs, invisibly shuffling money around. How many consumers did this model take into account in its assumptions about the economy? Millions? Hundreds of thousands? No, just one. One perfectly average or “representative” consumer operating perfectly rationally in the marketplace. Facing a crisis precipitated by the contagion of homeowner exuberance, fueled by the pathological recklessness of bond traders and bankers, abetted by inattentive government watchdogs, and leading to the deepest recession since the Great Depression, the Fed and other Western central banks found themselves fighting a crisis their models said could not happen.

This is an indictment not only of central bankers and the economics profession; nor merely of the Republicans whose doctrine abetted such intellectual malpractice; it is also an indictment of the Democrats who, bearing responsibility for making government work, allowed such a dreamland view of the world to drive government action in the national economy. They did so because over the course of 20 years they too had become believers in the efficient market hypothesis. Where housing and banking were concerned, there arose a faith-based economy: faith in rational individuals, faith in ever-rising housing values, and faith that

you

would not be the one left standing when the music stopped.

you

would not be the one left standing when the music stopped.

We are not, to be emphatically clear, anti-market. In fact, we are avid capitalists. Markets have an overwhelming benefit to human societies, and that is their unmatched ability to solve human problems. A modern understanding of economies sees them as complex adaptive systems subject to evolutionary forces. Those forces enable competition for the ability to survive and succeed as a consequence of the degree to which problems for customers are solved. Understood thus, wealth in a society is simply the sum of the problems it has managed to solve for its citizens. Eric Beinhocker calls this “information.” As Beinhocker notes, less developed “poor” societies have very few solutions available. Limited housing solutions. Limited medical solutions. Limited nutrition and recreation solutions. Limited information. Contrast this with a modern Western superstore with hundreds of thousands of SKUs, each representing a unique solution to a unique problem.

But markets are agnostic to what kind of problems they solve and for whom. Whether a market produces more solutions for human medical challenges or more solutions for human warfare—or whether it invents problems like bad breath for which more solutions are needed—

is wholly a consequence

of the construction of that market, and that construction will always be human made, either by accident or by design. Markets are meant to be servants, not masters.

is wholly a consequence

of the construction of that market, and that construction will always be human made, either by accident or by design. Markets are meant to be servants, not masters.

As we write, the Chinese government is making massive, determined, strategic investments in their renewable energy industry. They’ve decided that it’s better for the world’s largest population and second-largest economy to be green than not—and they are shaping the market with that goal in mind. By doing so they both reduce global warming

and

secure economic advantage in the future. We are captive, meanwhile, to a market fundamentalism that calls into question the right of government to act at all—thus ceding strategic advantage to our most serious global rival and putting America in a position to be poorer, weaker, and dirtier down the road. Even if there hadn’t been a housing collapse, the fact that our innovative energies were going into building homes we didn’t need and then securitizing the mortgages for those homes says we are way off track.

and

secure economic advantage in the future. We are captive, meanwhile, to a market fundamentalism that calls into question the right of government to act at all—thus ceding strategic advantage to our most serious global rival and putting America in a position to be poorer, weaker, and dirtier down the road. Even if there hadn’t been a housing collapse, the fact that our innovative energies were going into building homes we didn’t need and then securitizing the mortgages for those homes says we are way off track.

Now, it might be noted that for decades, through administrations of both parties, our nation

did

have a massive strategic goal of promoting homeownership—and that what we got for all that goal-setting was a housing-led economic collapse. But setting a goal doesn’t mean then going to sleep; it requires constant, vigilant involvement to see whether the goal is the right goal and whether the means of reaching the goal come at too great a cost. Homeownership is a sound goal. That doesn’t mean homeownership by any means necessary is a sound policy. Pushing people into mortgages they couldn’t truly afford and then opening a casino with those mortgages as the chips was not the only way to increase homeownership. What government failed to do during the housing boom was to

garden

—to weed out the speculative, the predatory, the fraudulent.

did

have a massive strategic goal of promoting homeownership—and that what we got for all that goal-setting was a housing-led economic collapse. But setting a goal doesn’t mean then going to sleep; it requires constant, vigilant involvement to see whether the goal is the right goal and whether the means of reaching the goal come at too great a cost. Homeownership is a sound goal. That doesn’t mean homeownership by any means necessary is a sound policy. Pushing people into mortgages they couldn’t truly afford and then opening a casino with those mortgages as the chips was not the only way to increase homeownership. What government failed to do during the housing boom was to

garden

—to weed out the speculative, the predatory, the fraudulent.

Conventional wisdom says that government shouldn’t try to pick winners in the marketplace, and that such efforts are doomed to failure. Picking winners may be a fool’s errand, but

choosing the game

we play is a strategic imperative. Gardeners don’t make plants grow but they do create conditions where plants can thrive and they do make judgments about what should and shouldn’t be in the garden. These concentration decisions, to invest in alternative energy or not, to invest in biosciences or not, to invest in computational and network infrastructure or not, are essential choices a nation must make.

choosing the game

we play is a strategic imperative. Gardeners don’t make plants grow but they do create conditions where plants can thrive and they do make judgments about what should and shouldn’t be in the garden. These concentration decisions, to invest in alternative energy or not, to invest in biosciences or not, to invest in computational and network infrastructure or not, are essential choices a nation must make.

This is not picking winners; it’s

picking games.

Public sector leaders, with the counsel and cooperation of private sector experts, can and must choose a game to invest in and then let the evolutionary pressures of market competition determine who wins

within

that game. DARPA (the Defense Advanced Research Projects Agency), NIST (the National Institute of Standards and Technology), NIH (National Institutes of Health), and other effective government entities pick games. They issue grand challenges. They catalyze the formation of markets, and use public capital to leverage private capital. To refuse to make such game-level choices is to refuse to have a strategy, and is as dangerous in economic life as it would be in military operations. A nation can’t “drift” to leadership. A strong public hand is needed to point the market’s hidden hand in a particular direction.

Markets as Machines vs. Markets as Gardenspicking games.

Public sector leaders, with the counsel and cooperation of private sector experts, can and must choose a game to invest in and then let the evolutionary pressures of market competition determine who wins

within

that game. DARPA (the Defense Advanced Research Projects Agency), NIST (the National Institute of Standards and Technology), NIH (National Institutes of Health), and other effective government entities pick games. They issue grand challenges. They catalyze the formation of markets, and use public capital to leverage private capital. To refuse to make such game-level choices is to refuse to have a strategy, and is as dangerous in economic life as it would be in military operations. A nation can’t “drift” to leadership. A strong public hand is needed to point the market’s hidden hand in a particular direction.

Understanding economics in this new way can revolutionize our approach and our politics. The shift from mechanistic models to complex ecological ones is not one of degree but of kind. It is the shift from a tradition that prizes fixity and predictability to a mindset that is premised on evolution. Compare two frames in capsule form:

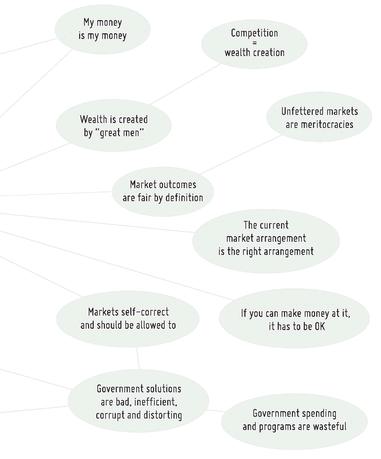

Machine view:

Markets are efficient, thus sacrosanct

Markets are efficient, thus sacrosanct

Garden view:

Markets are effective, if well tended

Markets are effective, if well tended

In the traditional view, markets are sacred because they are said to be the most efficient allocators of resources and wealth. Complexity science shows that markets are often quite inefficient—and that there is nothing sacred about today’s man-made economic arrangements. But complexity science also shows that markets are the most effective force for producing innovation, the source of all wealth creation. The question, then, is how to deploy that force to benefit the greatest number.

Machine view:

Regulation destroys markets

Regulation destroys markets

Garden view:

Markets need fertilizing and weeding, or else are destroyed

Markets need fertilizing and weeding, or else are destroyed

Traditionalists say any government interference distorts the “natural” and efficient allocation that markets want to achieve. Complexity economists show that markets, like gardens, get overrun by weeds or exhaust their nutrients (education, infrastructure, etc.) if left alone, and then die—and that the only way for markets to deliver broad-based wealth is for government to tend them: enforcing rules that curb anti-social behavior, promote pro-social behavior, and thus keep markets functioning.

Machine view:

Income inequality reflects unequal effort and ability

Income inequality reflects unequal effort and ability

Garden view:

Inequality is what markets naturally create and compound, and requires correction

Inequality is what markets naturally create and compound, and requires correction

Traditionalists assert, in essence, that income inequality is the result of the rich being smarter and harder working than the poor. This justifies government neglect in the face of inequality. The markets-as-garden view would not deny that smarts and diligence are unequally distributed. But in their view, income inequality has much more to do with the inexorable nature of complex adaptive systems like markets to result in self-reinforcing concentrations of advantage and disadvantage. This necessitates government action to counter the unfairness and counterproductive effects of concentration.

Machine view:

Wealth is created through competition and by the pursuit of narrow self-interest

Wealth is created through competition and by the pursuit of narrow self-interest

Garden view:

Wealth is created through trust and cooperation

Wealth is created through trust and cooperation

Where traditionalists put individual selfishness on a moral pedestal, complexity economists show that norms of unchecked selfishness kill the one thing that determines whether a society can generate (let alone fairly allocate) wealth and opportunity: trust. Trust creates cooperation, and cooperation is what creates win-win outcomes. High-trust networks thrive; low-trust ones fail. And when greed and self-interest are glorified above all, high-trust networks become low-trust.

See

: Afghanistan.

See

: Afghanistan.

Machine view:

Wealth = individuals accumulating money

Wealth = individuals accumulating money

Garden view:

Wealth = society creating solutions

Wealth = society creating solutions

One of the simple and damning limitations of traditional economics is that it can’t really explain how wealth gets generated. It simply assumes wealth. And it treats money as the sole measure of wealth. Complexity economics, by contrast, says that wealth is

solutions

: knowledge applied to solve problems. Wealth is created when new ideas—inventing a wheel, say, or curing cancer—emerge from a competitive, evolutionary environment. In the same way, the greatness of a garden comes not just in the sheer volume but also in the

diversity and usefulness

of the plants it contains.

solutions

: knowledge applied to solve problems. Wealth is created when new ideas—inventing a wheel, say, or curing cancer—emerge from a competitive, evolutionary environment. In the same way, the greatness of a garden comes not just in the sheer volume but also in the

diversity and usefulness

of the plants it contains.

In other words, money accumulation by the rich is not the same as wealth creation by a society. If we are serious about creating wealth, our focus should not be on taking care of the rich so that their money trickles down; it should be on making sure

everyone

has a fair chance—in education, health, social capital, access to financial capital—to create

new

information and ideas. Innovation arises from a fertile environment that allows individual genius to bloom and that amplifies individual genius, through cooperation, to benefit society. Extreme concentration of wealth kills prosperity in precisely the same way that untended weeds overrun and then kill gardens.

everyone

has a fair chance—in education, health, social capital, access to financial capital—to create

new

information and ideas. Innovation arises from a fertile environment that allows individual genius to bloom and that amplifies individual genius, through cooperation, to benefit society. Extreme concentration of wealth kills prosperity in precisely the same way that untended weeds overrun and then kill gardens.

MARKETS: Machinebrain View

MARKETS: Gardenbrain View

Other books

Her Dream Cowboy by Emily Silva, Samantha Holt

Isadora (Masters Among Monsters Book 2) by Ella Frank

Wrath of the Blue Lady by Odom, Mel

King City by Lee Goldberg

Nemecene: The Epoch of Redress by Kaz Lefave

The Willful Princess and the Piebald Prince by Robin Hobb

The Given by Vicki Pettersson

Before the Storm by Rick Perlstein

It'll Come Back... by Richardson, Lisa

100 Most Infamous Criminals by Jo Durden Smith